Banks and credit unions – not to mention their customers – have made their way through a gauntlet of disruptive trends over the past three years. Financial consumers have emerged with higher expectations of service and lower tolerance for frustration in their customer journeys. As customer preferences continue to evolve toward greater personalization, financial institutions that want to temper volatility in customer loyalty need to adopt strategies informed by continuous CX intel, then commit to acting on it.

Takeaways:

- Disruptive dynamics and challenges of the past 3 years have sparked numerous cumulative effects that threaten the customer experience.

- Financial consumers’ loyalty is conditional, as they are increasingly intolerant of service that doesn’t meet their heightened expectations.

- Financial institutions that haven’t adapted well to challenges of the past 3 years need to change their CX approach if they are to survive trends predicted for the near future.

Most of the C-level executives we talk to acknowledge that the last 3 years have been difficult to navigate for credit unions and banks. Has this been your reality?

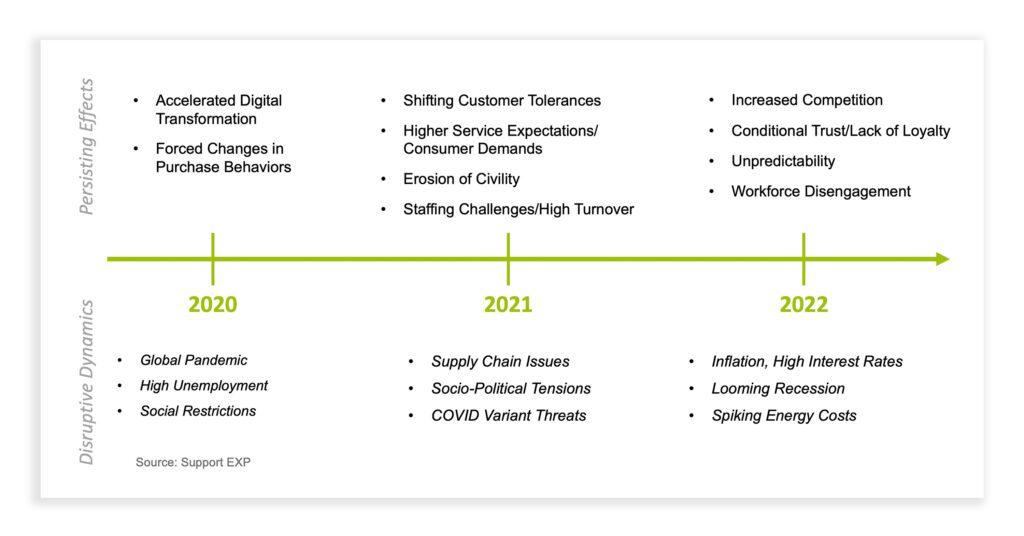

To affirm, here are just some of the disruptive forces at play in recent years:

Looking Back: Impact = CX Volatility!

What is often lost sight of is the impact these forces had on the consumer, and how consumers responded to them. The result has been nothing less than an unprecedented volatility in the customer experience!

At your organization, you may have noticed some of the effects correlated with these disruptive forces:

- Have your customers been acting and speaking with greater incivility?

- Are your customers less tolerant of service that doesn’t meet their expectations?

- Have you struggled to slow down customer attrition in the face of diminishing loyalty?

- Are you coping with a persistent talent shortage, unable to attract and retain frontline staff?

If you have navigated the challenges of the last 3 years in such a way that your key CX metrics (whether NPS, CSAT, CES), have recovered quickly from their impact…

If your teams, despite all the effects of these disruptive forces, have risen to the occasion – showing superior empathy skills when faced with frustrated or upset customers; providing reliable, personalized service no matter the channel or circumstance; staying with you and being engaged despite “the Great Resignation” and “quiet quitting”…

…then you just might be well positioned for tackling the challenges of 2023. No need for wholesale change if it “ain’t broke” – just build stronger.

Looking Forward: Evolving Demands – Impact Unknown

Now – looking forward, a host of macroeconomic, technological, regulatory and competitive forces loom, as charted in Deloitte’s 2023 Banking and Capital Markets Outlook. Chief among these, in the retail banking sector, are evolving customer preferences and greater demand for personalization. These are the realities banking executives will face in 2023. These are the forces that will have the greatest impact, near-term. How prepared are you to deal with them?

It would be a huge advantage to know what financial consumers’ preferences will be before your competition does (or even before the consumers know!). Given the rate at which those preferences change, the diversity of your customer base, the volatility of consumer mindsets, and the complexity of today’s financial problems, you need a strategy that enables you to respond quickly or take proactive steps to meet your customers’ demands and expectations.

The Real-World Strategies

What does a responsive or proactive approach look like? Here are three strategic CX imperatives, each illustrated by a real-world case of a credit union’s response to disruptive change:

1. Capture evolving customer expectations in your data, and get insights out of the data that you can act on.

The Short of It: This credit union prepared for its conversion to a new online and mobile banking platform by doubling down on the member feedback it was receiving from its digital channels. Rather than closing their ears to member complaints where service was falling short of expectations, they welcomed member input on their experiences with the new platform as a source of insight.

The Outcome: The credit union experienced a quick recovery in member satisfaction and loyalty following the disruption arising from the conversion. Member feedback provided the critical intel the credit union used to inform their strategy and take action to address issues with the new platform impacting their members the most.

2. Know what operational or process difficulties your customers are dealing with, and determine how to make it easier for them to do business with you.

The Short of It: This credit union was executing a merger with a similarly sized institution. They chose to shut off member feedback prior to the merger, anticipating a drop in member satisfaction related to the disruption. As predicted, members were frustrated with glitches during the systems conversion.

The Outcome: Instead of a quick recovery, member dissatisfaction persisted due to closed channels of communication throughout the transition – the credit union lacked meaningful intel about where to target their remedial resources and efforts. Lacking an avenue for feedback, members expressed their dissatisfaction by taking their business elsewhere – even after long years of membership in one of the merging businesses.

3. Know if you are delivering what customers need and want, with optimal value and efficiency.

The Short of It: In this case, credit union executives sought to drive greater member adoption of digital channels (online and mobile banking) for routine transactions. The credit union took the initiative in seeking feedback from their members on what digital banking features would be most valuable to them.

The Outcome: This credit union’s member-centric approach not only guided allocation of resources to priority product development, it improved operational efficiency by encouraging more members to use digital banking channels for routine transactions – with readily available human assistance when needed.

If there is clarity in Deloitte’s crystal ball, future success will hinge on keeping pace with evolving customer preferences and personalized service. As the above cases show, this can only be done through an always-on, real-time source of customer intel. When you have in place a system that alerts you immediately when customer satisfaction is being compromised, you can act quickly, intentionally and intelligently. The sooner you can act, the less work you’ll have to do to stay in your customers’ good graces if (or when?) things don’t go as planned.

Customer satisfaction starts at the top, with every strategic decision made to advance your bank or credit union’s mission. But executing that strategy is just the first step. If you’re not actively measuring your customers’ reaction to the change, and interpreting the data correctly, you won’t be able to respond in turn with the right action to save the relationship from fatal customer dissatisfaction!

Of course, the actions that will lead to customer satisfaction are not always intuitive or a matter of common sense. That’s why it is so important to capture your customers’ reactions to events in real time, and in every moment of time when strategic decisions are playing out – until turbulent customer relationships settle back to a state of satisfaction.

A Time of Conviction

The authors of Deloitte’s 2023 Banking Outlook observe that, “The pandemic tested banking leaders’ conviction, and it is about to be tested again.” It takes courage to commit to a customer-centric process when faced with uncertainty and rapid change, but banking executives willing to act with conviction will be long-term leaders – not just of their own organizations, but of their industry.

We can help – not just by driving change but by ensuring that the change you make in 2023 is intentional, intel-informed, and taking you precisely where you want to go.